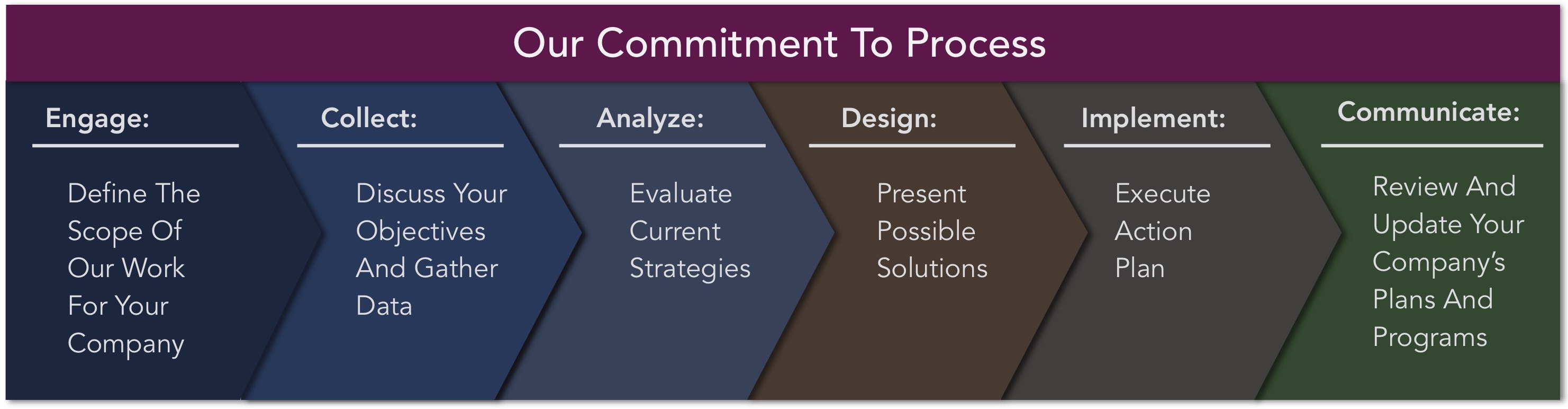

We adhere to a philosophy of “process before product” in every aspect of the work we perform for your business. After learning and understanding your objectives and carefully evaluating possible strategies for your company, we will implement those strategies with appropriately suitable financial products. We will regularly review your business’s strategies as your objectives or circumstances change.

Employer-Sponsored Retirement Plans

An employer-sponsored qualified plan makes possible tax-favored retirement savings, benefiting employees and the sponsoring employer. Depending on your company’s structure, employee demographics and other factors, we will help to design, implement and maintain your qualified retirement plan. We can assist with a variety of types of plans, including:

- 401K) plans

- Roth 401(k) plans

- Safe-harbor 401(k) plans

- Cash-balance plans

- New-comparability plans

- SIMPLE-IRA plans

- SEP plans

- Profit-sharing plans

- Defined-benefit plans

- Multiple-employer plans (MEPs)

For more details on our retirement plan services, please click here.

Before deciding whether to retain assets in a 401(k) or roll over to an IRA, an investor should consider various factors including, but not limited to, investment options, fees and expenses, services, withdrawal penalties, protection from creditors and legal judgements, required minimum distributions and possession of employer stock. Please view the Investor Alerts section of the FINRA website for additional information.

Group Insurance Plans

Employee Benefits – Group Insurance Plans

We provide full-service group health insurance for small, medium and large businesses, non-profit organizations and other entities:

- Group health insurance plans

- Group short-term and long-term disability insurance plans

- Group life insurance plans

- Group dental and vision plans

Our commitment to you and your company includes:

- Plan design

- Quoting and proposal analysis

- Affordable Care Act compliance

- Implementation

- Renewal

- Open enrollment:

- Group meetings

- One-on-one customized electronic enrollments

- Spanish language services

- Customized employee benefit video presentations

- Quarterly on-site service meetings

- Sophisticated, cost-saving and benefit enhancing strategies:

- Medical expense reimbursement plans (MERP)

- High-deductible health plans (HDHP)

- Partial self-funding

- Health savings accounts (HSA)

- Healthcare reimbursement arrangements (HRA)

- Gap coverage

The cost and availability of life insurance depend on factors such as age, health, and the type and amount of insurance purchased. Before implementing a strategy involving life insurance, it would be prudent to make sure that you are insurable by having the policy approved. As with most financial decisions, there are expenses associated with the purchase of life insurance. Policies commonly have mortality and expense charges. In addition, if a policy is surrendered prematurely, there may be surrender charges and income tax implications.

Executive Compensation and Insurance Plans

Executive Deferred-Compensation Plans

Contributions to qualified plans and individual retirement accounts (IRAs) are subject to limits defined by the tax code. Also, qualified plans are subject to coverage and nondiscrimination testing that may limit both employee and employer contributions to the plans, and highly compensated employees may subject to a cap on Social Security benefits.

A non-qualified deferred-compensation plan can augment your and your executives’ other retirement plans and are generally not subject to the tax and compliance-related constraints described above. It may also bolster your executive recruiting efforts.

Executive Disability Insurance

During your working years, your income-earning ability may be your greatest asset. If that ability is interrupted due to a sickness or accident, your financial security may be imperiled. Group disability insurance plans may provide a basic level of coverage, but company owners and executives often have unique needs, occupational specialties and elevated financial circumstances. We can help secure your financial security by designing specialized plans of insurance:

- Individual disability income insurance

- Integrated individual and group disability insurance plans

- Catastrophic disability insurance

- Overhead expense insurance

- Disability buyout insurance

- Debt-reducing term disability insurance

- Pension-completing disability insurance

- Coverage for highly specialized occupations.

The cost and availability of life insurance depend on factors such as age, health, and the type and amount of insurance purchased. Before implementing a strategy involving life insurance, it would be prudent to make sure that you are insurable by having the policy approved. As with most financial decisions, there are expenses associated with the purchase of life insurance. Policies commonly have mortality and expense charges. In addition, if a policy is surrendered prematurely, there may be surrender charges and income tax implications.

Flexible-Spending Programs, Supplemental Insurance and Other Voluntary Benefits

Cafeteria and Flexible-Spending Plans

A cafeteria plan is a voluntary, employer-sponsored program for employees to save a portion of their income, pre-tax, to be used to pay for qualified medical or dependent care expenses incurred during their benefit plan year. Employee participation in a cafeteria plan may also reduce employer payroll tax liabilities. Our allied third-party administrators will provide plan documents, administration, guidance and reporting. Services may include direct deposits of claims reimbursements and/or personal debit cards.

- Full-scope cafeteria plan (pre-tax insurance premiums, medical flexible-spending account, dependent daycare and transportation)

- Limited-scope flexible-spending plan (compatible with HSA medical plans)

- Premium-only plan (pre-tax insurance premiums only)

- SIMPLE cafeteria plan (for small employers)

Voluntary Benefits

Voluntary supplemental plans enable your employees to tailor their benefits to the specific needs of themselves and their families. Benefits are generally paid in cash to the covered person, and plans are portable. Premiums for some types of supplemental plans may be paid on a pre-tax basis through your company’s cafeteria plan. Common types of voluntary supplemental plans include:

- Critical illness plans (cancer, heart disease, stroke)

- Accident-benefit plans

- Short-term disability plans

- Life insurance

- Long-term care insurance

- Payroll-deduction 529 college-savings plans.

The cost and availability of life insurance depend on factors such as age, health, and the type and amount of insurance purchased. Before implementing a strategy involving life insurance, it would be prudent to make sure that you are insurable by having the policy approved. As with most financial decisions, there are expenses associated with the purchase of life insurance. Policies commonly have mortality and expense charges. In addition, if a policy is surrendered prematurely, there may be surrender charges and income tax implications.

Buy-Sell and Key-Person Insurance

Buy-Sell Insurance

A well-crafted buy-sell agreement for your business continuity plan will specify the circumstances in which your or your partners’ ownership of the business will be transferred or sold. It sets forth the terms of sale: value, valuation methods and funding options. The agreement becomes a contractual obligation the moment you affix your signature to it, so it makes sense to secure the funding instruments before it is executed.

We will work with your attorneys and CPAs to develop business continuity and success plans and to secure the most cost-effective funding solutions to ensure the timely and efficient transfer of ownership of your share of the business:

- Buy-sell life insurance

- Disability buy-out insurance

Key-Person Insurance

Does your business success depend on the expertise, experience or leadership of key individuals? Would the loss of any of them (from death, serious illness or accident) affect the operation, viability or worth of your company? Key-person insurance provides capital to help sustain the business during the transition that follows such a loss. Overhead insurance provides an income stream to help cover operational expenses during the recovery of an owner or key-person following a disabling sickness or accident.

Key-person and overhead insurance plans include:

- Key-person term life insurance

- Key-person universal life insurance

- Key-person disability insurance

- Key-person disability overhead insurance.

The cost and availability of life insurance depend on factors such as age, health, and the type and amount of insurance purchased. Before implementing a strategy involving life insurance, it would be prudent to make sure that you are insurable by having the policy approved. As with most financial decisions, there are expenses associated with the purchase of life insurance. Policies commonly have mortality and expense charges. In addition, if a policy is surrendered prematurely, there may be surrender charges and income tax implications.

Overhead-Continuity and Pension-Completion Insurance

Overhead Continuity Insurance

If you become disabled, the day-to-day expenses of running your business will continue and can quickly add up. Before long, these expenses may force you to consider layoffs or even shutting down your business. Consider overhead expense insurance, which covers the normal, necessary and customary expenses associated with the operation of your business, including rent, mortgage, utilities and more. It can provide reimbursement for up to 100% of your expenses every month and can make the difference between returning to a viable business and returning to no business at all.

- Overhead expense insurance for businesses

- Overhead expense insurance for medical practices

- Overhead expense insurance for professional practices

Pension-Completion Disability Insurance

If a disability, from an accident or illness, occurs while one is accumulating a retirement plan, the results can be catastrophic. Suddenly, with no income, the disabled can no longer contribute to his or her retirement plan. A disability doesn’t just create immediate financial troubles, the future becomes uncertain as well.

This plan can be designed to pay the equivalent of the balance of the contributions anticipated by the participant. The benefit is paid out as a lump sum and is paid directly to the insured. With the guidance of a professional planner, the insured may elect to invest the benefit into funds similar to his or her retirement plan or to an annuity or other investment instrument. Pension Completion Disability Insurance will keep the disabled focused on the tasks at hand, providing for his or her family and recovering from his or her recent setback.

The cost and availability of life insurance depend on factors such as age, health, and the type and amount of insurance purchased. Before implementing a strategy involving life insurance, it would be prudent to make sure that you are insurable by having the policy approved. As with most financial decisions, there are expenses associated with the purchase of life insurance. Policies commonly have mortality and expense charges. In addition, if a policy is surrendered prematurely, there may be surrender charges and income tax implications.

Special-Risk Insurance Programs

Special-Risk Disability and Life Insurance

Business executives and individuals in highly specialized and very-high-income occupations may desire disability protection beyond that which is available from most carriers.

We can help secure high-limit disability coverage for various specialized occupations:

- High-income business owners and executives

- Physicians and surgeons

- Performers and entertainment executives

- Professional athletes

- Securities and commodities traders and brokers

- Attorneys and judges

- Chiropractors

- Pilots

- Blue- and gray-collar occupations

Special circumstances may elevate the level of financial risk for which life insurance is a solution. Overseas travel may expose an executive to special risks, or a business owner who is party to a buy-sell agreement may be medically uninsurable for traditional life insurance. For such needs, we can provide:

- Accident-only life insurance

- High-limit accident life insurance

The cost and availability of life insurance depend on factors such as age, health, and the type and amount of insurance purchased. Before implementing a strategy involving life insurance, it would be prudent to make sure that you are insurable by having the policy approved. As with most financial decisions, there are expenses associated with the purchase of life insurance. Policies commonly have mortality and expense charges. In addition, if a policy is surrendered prematurely, there may be surrender charges and income tax implications.

Commercial Lines: General Liability, Property & Casualty and Captive Insurance Programs

Commercial Lines Insurance For Your Business

Through our affiliation with AssuredPartners, Inc., we deliver custom solutions for all of your property and casualty needs, including plan design and risk analysis, extensive market choices, loss control education and training, and developing consumer-driven programs.

- General liability insurance

- Workers’ compensation insurance

- Risk mitigation / safety programs

- Officers and directors insurance

- Professional liability insurance

- Commercial auto insurance

- Fidelity bonds

The substantial resources of AssuredPartners, Inc., locally and nationally, enable us to define your company’s risks and to design solutions to limit and transfer those risks through the acquisition of appropriate insurance products and programs. Benefits of choosing AssuredPartners for your company's commercial lines of insurance and related programs include:

- Risk analysis and solutions

- Local, national and international capabilities

- Policy review

- Extensive underwriting experience

- Access to extensive insurance markets and carriers

- Exceptional service.

The cost and availability of life insurance depend on factors such as age, health, and the type and amount of insurance purchased. Before implementing a strategy involving life insurance, it would be prudent to make sure that you are insurable by having the policy approved. As with most financial decisions, there are expenses associated with the purchase of life insurance. Policies commonly have mortality and expense charges. In addition, if a policy is surrendered prematurely, there may be surrender charges and income tax implications.

Fiduciary and Compliance Support

We support our plan sponsor clients to help them meet their fiduciary obligations under ERISA while assisting participants to save and invest toward their retirement goals.

- Investment Policy Statement review, analysis, and drafting assistance

- Investment due diligence analysis, fund ranking and recommendations

- Provider searches and fee benchmarking analysis and negotiation

- Plan design review and consulting

- Annual fiduciary gap analysis, education, review, and documentation

- ERISA 404(a) and 404(c) fiduciary guidance

- Regulatory/legislative updates and interpretation

- Quarterly market summary and monthly employer newsletters

- Employee meetings and communications

- Individual financial consulting

- Deferred compensation plan consulting

When working in a Registered Investment Advisory capacity, Vantage Financial Group, Inc. will become a co-fiduciary to your retirement plan as it relates to the selection and monitoring of the investments. These services may be in either a 3(21) or a 3(38) fiduciary role.

Benefits Administration and Communication Support

Employee Communications

We provide professional and consistent communications to your employees throughout the entire enrollment process to ensure that they understand and appreciate their benefits.

- Pre-enrollment communications (print, digital and online)

- Group meetings

- One-on-one meetings

- Employee benefits consulting

- Electronic enrollment system

Human Resources Information System

We provide proprietary technology that assists with your employee benefits management and your basic Human Resource information tasks. This proprietary system differentiates us from other insurance agencies by providing clients with an end-to-end solution to help manage the ever increasing complexity of benefits administration. This proprietary single-entry, multiple-company interface (SEMCI) automates the employee benefits transactions with a client’s insurance carriers and other benefits vendors. The system integration and connectivity gives an employer the ability to devote more time to increasing profitability rather than struggling with employee benefits paperwork.

ERISA, FMLA and COBRA Compliance

Employers face strict deadlines for disclosing benefit plan information to all eligible employees. And all plan sponsors and plan administrators with ERISA plans must follow a strict fiduciary code of conduct. Failure to comply with ERISA requirements can be extremely costly. Consequences for non-compliance may include government penalties, even employee lawsuits.

For companies with 50 or more employees, the Family & Medical Leave Act (FMLA) entitles eligible employees the right to take unpaid, job-protected leave for specified family and medical reasons. During said leave group health insurance coverage must continue under the same terms and conditions that would apply if the employee had not taken leave. Created in 1993, FMLA permits employees up to 12 weeks of excused absence from their jobs every year. It was enacted to aid employees in balancing work and personal obligations in times of crisis.

COBRA stands for the Consolidated Omnibus Budget Reconciliation Act, which became law in 1986. COBRA gives your employees the right to choose to temporarily keep the group health insurance benefits that they would otherwise lose after reducing working hours, quitting, or being involuntarily terminated. It also lets family members choose to keep health insurance after a job loss or other qualifying event. COBRA administration is a complex process, governed by constantly changing rules and regulations, and virtually every aspect of COBRA is extremely time-sensitive, so prompt and proper actions are critical.

Through our allied service providers, we can provide individual or packaged compliance services in each of these areas.

Healthcare Reform Guidance

We are committed to providing up-to-date guidance on regulatory requirements of the Affordable Care Act. Our HR-360 service, provided on a complementary basis to clients, is a robust source of guidance, explanations and documents pertaining to the ACA.

Professional Employer Organizations (PEOs)

Professional employer organizations (PEOs) enable businesses to outsource the management of human resources, employee benefits, payroll and workers' compensation insurance. PEO clients focus on their core competencies to maintain and grow their bottom line. A PEO delivers these services by establishing and maintaining an employer relationship with the employees at the client's worksite and by contractually assuming certain employer rights, responsibilities, and risk. We can assist with procuring PEO services for your business:

- Full-service PEOs

- Unbundled PEOs (a la carte services)