We adhere to a philosophy of “process before product” in every aspect of the work we perform for you and your family. After learning and understanding your objectives and carefully evaluating possible strategies, we will implement your plan with appropriately suitable financial products. We will regularly review and update your plan as your objectives or circumstances change.

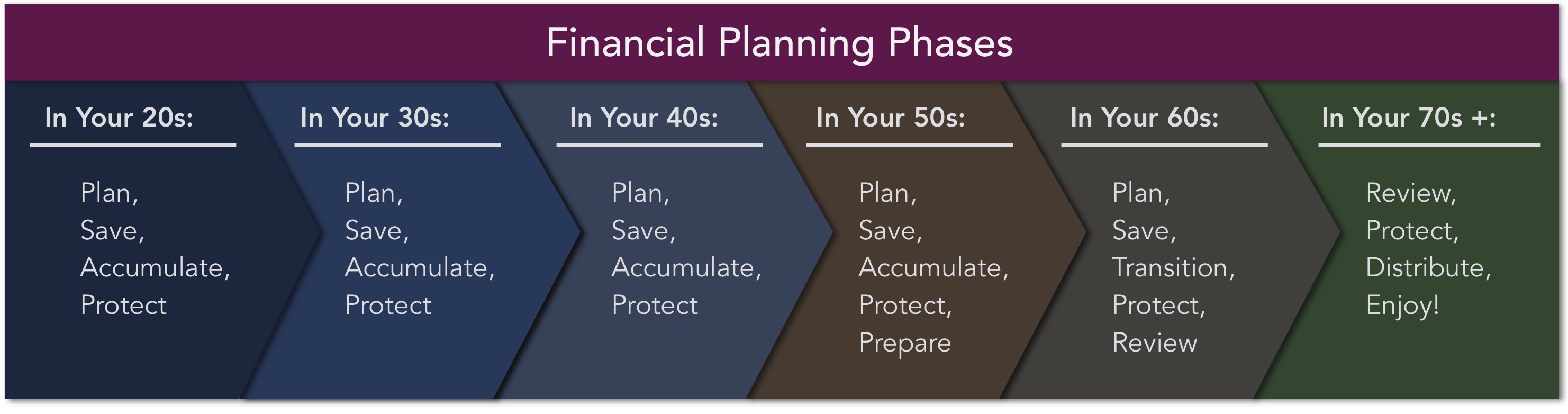

In Your Twenties...

Personal Investment Accounts

Personal and Family Financial Planning – In Your Twenties

Consider taking these financial steps in your twenties:

- Create a budget. Figure out where you stand: how much you earn, how much you owe and how much you regularly spend. Then create your budget and stick to it.

- Pay off consumer debt. Pay off a credit card as soon as possible to reduce your interest payment. If can't pay cards off quickly, try a consolidation loan.

- Start a savings program. Make it a habit to save and invest. Contributing to an employer retirement plan that offers the benefit of tax-deferred growth potential is a good first step.

- Determine personal insurance needs. Accidents and illness can be financially devastating. Protect against these risks with health, disability and life insurance, personally or through your employer.

- Protect belongings with insurance. Obtain a homeowner's policy or renter's insurance as an inexpensive way to protect your possessions against theft or fire.

- Create a Living Will. If you should become seriously ill, a living will can assist your family in making medical decisions according to your wishes.

In Your Thirties...

Personal and Family Financial Planning – In Your Thirties

Consider taking these financial steps in your thirties:

Save for retirement. 401(k) and 403(b) plans through your employer allow you to invest funds in a tax-advantaged and regular way. Familiarize yourself with tax aspects of your retirement plan options.

- Build a portfolio using mutual funds. Mutual funds can be a smart way to invest while minimizing the associated with owning individual stocks and bonds. Work with an advisor to find funds that match your needs and goals.

- Begin an education savings plan. If you have children, or plan to, begin saving now for their education. With education costs rising faster than general inflation, starting early is important for building up a fund. Consider tax-advantaged education-savings plans like 529 accounts.

- Pay off consumer debt. Paying off high-interest debt is the first way to begin saving. Pay off a credit card as soon as possible to avoid paying monthly interest.

- Utilize benefits offered by your employer. Make sure you're using your employee benefits to your advantage, including retirement plans, disability insurance, health coverage and voluntary options. Also consider the benefits of your employer’s flexible-spending (cafeteria) program.

- Review your personal insurance needs. Review your coverage for liability, health, life and disability insurance. Do you have enough coverage for yourself and your family in case of emergency?

- Anticipate housing needs. Consider a separate savings plan to finance moving or expansion to accommodate a growing family or aging parents.

- Name a guardian for your children. Protect your children by legally naming the person responsible for them should you and your partner die.

- Review and update your wills. Keep your wills up to date to reflect changes in your family status, assets you own and your preferences

In Your Forties...

Personal and Family Financial Planning – In Your Forties

Consider taking these financial steps in your forties:

- Diversify your investments. Expand your investment options to provide a mix of higher-return and more secure investments according to your plans for retirement.

- Utilize benefits offered by your employer. Make sure you're using your employee benefits to your advantage, including retirement plans, disability insurance, health coverage and voluntary options. Also consider the benefits of your employer’s flexible-spending (cafeteria) program.

- Review your personal insurance needs. Review your coverage for liability, health, life and disability insurance to be sure they are properly aligned with your current circumstances and objectives.

- Continue to build education savings funds. If you have children, continue saving regularly for their education. Consider tax-advantaged education-savings plans like 529 accounts.

- Develop an estate plan. A plan for your property and assets can help ensure that more of the earnings you've accumulated will go to your children or other beneficiaries.

- Review and update your wills. Keep your wills up to date to reflect changes in your family status, assets you own and your preferences.

- Consider establishing trusts. Planning now to establish trusts for your children or loved ones can be a way to pass along their inheritance with less of a tax burden while potentially avoiding probate.

- Review business agreements and transfer arrangements. If you have a business, make arrangements for a fair and predictable transfer of your business should you die, become disabled or wish to move on.

In Your Fifties...

Personal and Family Financial Planning – In Your Fifties

Consider taking these financial steps in your fifties:

- Evaluate and review retirement plans. Evaluate your retirement savings and expand your investment options, if needed, to balance future growth with current income.

- Diversify your investments. Expand your investment options to provide a mix of higher-return and more secure investments according to your plans for retirement.

- Consider annuities. Annuities are insurance products that can guarantee you a fixed income after you retire.They can be a supplement to other savings plans. (Guarantees are backed by the claims-paying ability of the insurance company.)

- Utilize benefits offered by your employer. Make sure you're using your employee benefits to your advantage, including retirement plans, disability insurance, health coverage and voluntary options. Also consider the benefits of your employer’s flexible-spending (cafeteria) program.

- Review your personal insurance needs. Review your coverage for liability, health, life and disability insurance to be sure they are properly aligned with your current circumstances and objectives.

- Think about long-term care. Plan your savings and insurance to help protect yourself or your spouse should either of you require health care for an extended period.

- Review your estate plan. Work with an advisor to develop or review a plan for your property and assets, including your wills, trusts, liquidity of assets and gifting.

- Review and update your wills. Keep your wills up to date to reflect changes in your family status, assets you own and your preferences.

- Consider establishing trusts. Planning now to establish trusts for your children or loved ones can be a way to pass along their inheritance with less of a tax burden while potentially avoiding probate.

- Review business agreements and transfer arrangements. If you have a business, make arrangements for a fair and predictable transfer of your business should you die, become disabled or wish to move on.

In Your Sixties...

Personal and Family Financial Planning – In Your Sixties

Consider taking these financial steps in your sixties:

- Re-evaluate budget and cash flow needs. Creating a budget is crucial to fulfilling your plans for retirement.Be sure to plan on a reserve for emergency situations when evaluating your needs.

- Review your investments and retirement plans. Evaluate your retirement savings, and examine if adjustments should be made in favor of more potentially lower-volatility investments. Begin planning for when your investments should produce cash flow for your living needs.

- Consider annuities. Annuities are insurance products that can guarantee you a fixed income after you retire.They can be a supplement to other savings plans. (Guarantees are backed by the claims-paying ability of the insurance company.)

- Utilize benefits offered by your employer. If you’re still working, make sure you're using your employee benefits to your advantage, including retirement plans, disability insurance, health coverage and voluntary options. Also consider the benefits of your employer’s flexible-spending (cafeteria) program.

- Consider part-time employment. Depending on your plans and circumstances, you can supplement your savings with part-time employment. Volunteer work can also help you by building a support network within your community.

- Review your personal insurance needs. Review your coverage for liability, health, life and disability insurance to be sure they are properly aligned with your current circumstances and objectives.

- Make sure your long-term care needs are met. Plan and discuss your desires and needs for possible long-term healthcare needs with your family.

- Supplement Medicare. Medicare may not be enough to provide the level of care you need. Work with an agent to determine an affordable level of coverage to appropriately supplement your Medicare benefits.

- Review your estate plan. Work with an advisor to develop or review a plan for your property and assets, including your wills, trusts, liquidity of assets and gifting.

- Review and update your wills. Keep your wills up to date to reflect changes in your family status, assets you own and your preferences.

- Review your trusts. Trusts for your children or loved ones can be a way to pass along their inheritance with less of a tax burden while potentially avoiding probate. Be sure they are still aligned with your objectives.

- Review business agreements and transfer arrangements. If you have a business, make arrangements for a fair and predictable transfer of your business should you die, become disabled or wish to move on.

In Your Seventies and Beyond...

Personal and Family Financial Planning – In Your Seventies

Consider taking these financial steps in your seventies:

Re-evaluate budget and cash flow needs. Creating a budget is crucial to fulfilling your plans for retirement. Be sure to plan on a reserve for emergency situations when evaluating your needs.

- Review your investments. Evaluate your retirement savings, and examine if they are properly aligned with your income needs and tolerance for risk.

- Consider volunteerism. Volunteerism can help you maintain a support network within your community while providing rewarding and stimulating interaction with others.

- Make sure your long-term care needs are met. Plan and discuss your desires and needs for possible long-term healthcare needs with your family.

- Supplement Medicare. Medicare may not be enough to provide the level of care you need. Work with an agent to determine an affordable level of coverage to appropriately supplement your Medicare benefits.

- Review your estate plan. Work with an advisor to develop or review a plan for your property and assets, including your wills, trusts, liquidity of assets and gifting.

- Review and update your wills. Keep your wills up to date to reflect changes in your family status, assets you own and your preferences.

- Review your trusts. Trusts for your children or loved ones can be a way to pass along their inheritance with less of a tax burden while potentially avoiding probate. Be sure they are still aligned with your objectives.

- Review business agreements and transfer arrangements. If you have a business, make arrangements for a fair and predictable transfer of your business should you die, become disabled or wish to move on.

- Consider your charitable gifting inclinations. Charitable gifting can be a meaningful part of your estate and legacy planning objectives. Consider opportunities to transfer assets to causes that are important to you.