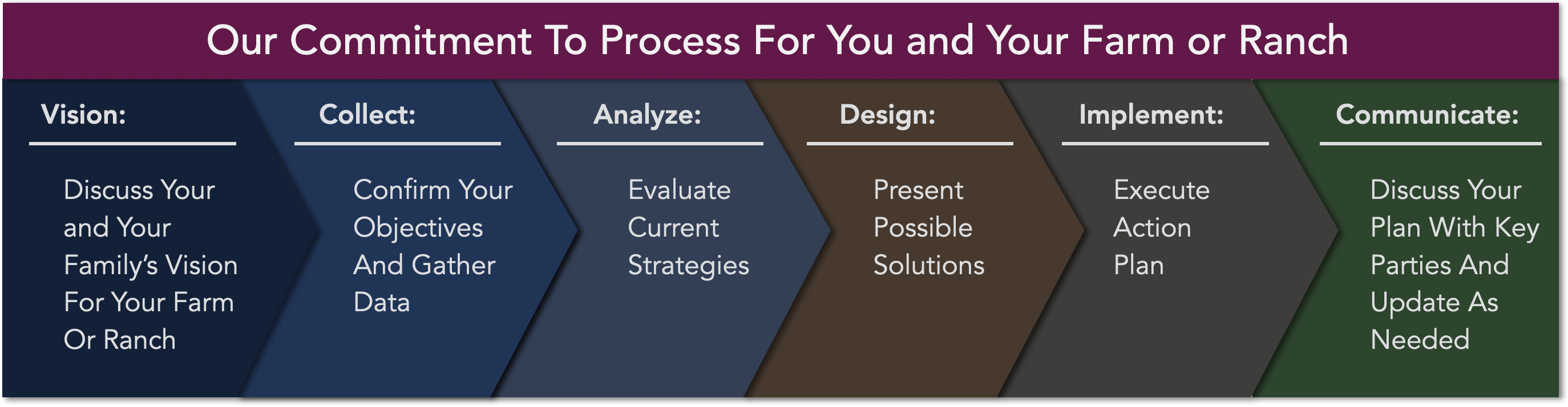

We adhere to a philosophy of “process before product” in every aspect of the work we perform for your Farm or Ranch. After learning and understanding your objectives and carefully evaluating possible strategies for you and your family, we can implement those strategies with appropriately suitable financial products. We will regularly review your strategies as your objectives or circumstances change.

Landowner Succession Planning

Creating the path to successfully pass the farm, ranch or agri-business to the next generation.

- Your vision for the future of your farm or ranch

- Circumstances that could initiate a transfer (retirement, illness or injury, death, other)

- Questions about control, operational roles, and ownership

- Financials

- Risks

- Documents

- Discussing and communicating the plan

For our list of suggested topics and questions, please click here.

Business Planning

Supporting the objective for current and future profitability for your farm, ranch, or agri-business.

- Employer-sponsored retirement plans (click here).

- Group health insurance plans

- Group short-term and long-term disability insurance plans

- Group life insurance plans

- Group dental and vision plans

Our commitment to you and your farm, ranch, or agri-business includes:

- Plan design

- Quoting and proposal analysis

- Affordable Care Act compliance

- Implementation

- Renewal

- Open enrollment:

- Group meetings

- Virtual meetings

- Customized electronic enrollments

- Spanish language services

- Customized employee benefit video presentations

- Sophisticated, cost-saving and benefit enhancing strategies:

- High-deductible health plans (HDHP)

- Partial self-funded / level-funded plans

- Health savings accounts (HSAs)

- Flexible-spending accounts (FSAs)

- Healthcare reimbursement arrangements (HRAs)

- Gap coverage

The cost and availability of life insurance depend on factors such as age, health, and the type and amount of insurance purchased. Before implementing a strategy involving life insurance, it would be prudent to make sure that you are insurable by having the policy approved. As with most financial decisions, there are expenses associated with the purchase of life insurance. Policies commonly have mortality and expense charges. In addition, if a policy is surrendered prematurely, there may be surrender charges and income tax implications.

Risk Management

Key-Person Considerations

Does the success of your farm or ranch depend on the expertise, experience or leadership of key individuals? Would the loss of any of them (from death, serious illness or accident) affect the operation, viability or worth of your farm or ranch? Key-person insurance provides capital to help sustain the business during the transition that follows such a loss. Overhead insurance provides an income stream to help cover operational expenses during the recovery of an owner or key-person following a disabling sickness or accident.

Key-person and overhead insurance plans include:

- Key-person term life insurance

- Key-person universal life insurance

- Key-person disability insurance

- Key-person disability overhead insurance.

Sickness or Accidents

During your working years, your income-earning ability may be one of your greatest assets. If that ability is interrupted due to a sickness or accident, your financial security may be imperiled. Group disability insurance plans may provide a basic level of coverage, but ranch or farm owners and agri-business owners often have unique needs, occupational specialties and elevated financial circumstances. We can help secure your financial security by designing specialized plans of insurance:

- Individual disability income insurance

- Integrated individual and group disability insurance plans

- Catastrophic disability insurance

- Overhead expense insurance

- Disability buyout insurance

- Debt-reducing term disability insurance

- Pension-completing disability insurance

- Coverage for highly specialized occupations.

The cost and availability of life, disability, or long-term care insurance depend on factors such as age, health, and the type and amount of insurance purchased. Before implementing a strategy involving life insurance, it would be prudent to make sure that you are insurable by having the policy approved. As with most financial decisions, there are expenses associated with the purchase of life insurance. Policies commonly have mortality and expense charges. In addition, if a policy is surrendered prematurely, there may be surrender charges and income tax implications.

Long-Term Care

Long-term care (LTC) is the term used to describe a variety of services in the area of health, personal care, and social needs of persons who are chronically disabled, ill or infirm. Depending on the needs of the individual, long-term care may include services such as nursing home care, assisted living, home health care, or adult day care.

Who Needs Long-Term Care?

The need for long-term care is generally defined by an individual's inability to perform the normal activities of daily living (ADL) such as bathing, dressing, eating, toileting, continence, and moving around. Conditions such as immune-deficiency conditions, spinal cord or head injuries, stroke, mental illness, Alzheimer's disease or other forms of dementia, or physical weakness and frailty due to advancing age can all result in the need for long-term care.

While the need for long-term care can occur at any age, older individuals are the typical recipients of such care.

Paying for Long-Term Care - Personal Resources

Much long-term care is paid for from personal resources:

- Out-of-Pocket: Expenses paid from personal savings and investments.

- Reverse Mortgage: Certain homeowners may qualify for a reverse mortgage, allowing them to tap the equity in the home while retaining ownership.

- Accelerated Death Benefits: Certain life insurance policies provide for "accelerated death benefits" (also known as a living benefit) if the insured becomes terminally or chronically ill.

- Private Health Insurance: Some private health insurance policies cover a limited period of at-home or nursing home care, usually related to a covered illness or injury.

- Long-Term Care Insurance: Private insurance designed to pay for long-term care services, at home or in an institution, either skilled or unskilled. Benefits will vary from policy to policy.

Paying for Long-Term Care - Government Resources

Long-term care that is paid for by government comes from two primary sources:

- Medicare: Medicare is a health insurance program operated by the federal government. Benefits are available to qualifying individuals age 65 and older, certain disabled individuals under age 65, and those suffering from end-stage renal disease. A limited amount of nursing home care is available under Medicare Part A, Hospital Insurance. An unlimited amount of home health care is also available, if made under a physician's treatment plan.

- Medicaid: Medicaid is a welfare program funded by both federal and state governments, designed to provide health care for the truly impoverished. Eligibility for benefits under Medicaid is typically based on an individual's income and assets; eligibility rules vary by state.

The cost and availability of life, disability, or long-term care insurance depend on factors such as age, health, and the type and amount of insurance purchased. Before implementing a strategy involving life insurance, it would be prudent to make sure that you are insurable by having the policy approved. As with most financial decisions, there are expenses associated with the purchase of life insurance. Policies commonly have mortality and expense charges. In addition, if a policy is surrendered prematurely, there may be surrender charges and income tax implications.

Financial Independence

Our Time-Segmented Approach To Financial Independence in Retirement

Our time-segmented approach to financial independence is a strategy that seeks to achieve three primary goals:

- Create income

- Mitigate risk

- Address inflation concerns

We apportion a person's investment and other income assets into time-segmented categories:

- Known / Income Sources

- Fixed-Income Sources (Near-Term)

- Balanced Future Income Sources (Intermediate-Term)

- Long-Term Growth

Known / Confident Income Sources

The first step in developing your plan is to assess known and/or highly confident sources of income cash flow, such as:

- Social Security

- Pensions

- Annuities

- Rental Income

Fixed-Income Segment

The Fixed-Income Segment is designed to be spent down over 5 to 7 years, thus "buying time" for the Balanced Segment to potentially grow. This category is usually invested in safe, sometimes guaranteed, investments.

Balanced Segment

The Balanced Segment is a bridge between the Fixed-Income Segment and Long-Term Growth Segment. This segment is designed to replenish the Fixed-Income Segment, resulting in additional time for your long- term investments to potentially grow.

Long-Term Growth Segment

The Long-Term Growth Segment is designed for 15-25 years of growth. Since the other Segments have provided time, this Segment is intended to grow untouched for many years.

Estate Planning for Farm or Ranch Owners

Estate Conservation and Wealth Transfer Planning

Generally, the goals of estate planning are to provide for financial security in life and to maximize - given your goals and objectives - the estate for your family and other heirs following death. To fully leverage estate preservation opportunities and develop strategies to help achieve distribution objectives, we will work with you and your attorneys in the following areas:

- Will and trust design strategies

- Property ownership considerations

- Beneficiary designation reviews

- Estate tax reduction techniques

- Insurance analysis

- Qualified plan distribution alternatives

- Employee stock option optimization

- Family-gifting strategies

- Charitable-gifting strategies.

The cost and availability of life insurance depend on factors such as age, health, and the type and amount of insurance purchased. Before implementing a strategy involving life insurance, it would be prudent to make sure that you are insurable by having the policy approved. As with most financial decisions, there are expenses associated with the purchase of life insurance. Policies commonly have mortality and expense charges. In addition, if a policy is surrendered prematurely, there may be surrender charges and income tax implications.